Santalucía Impulsa, the Santalucía Group's open innovation and entrepreneurship ecosystem, has prepared, together with El Referente, the Insurtech Ecosystem Report 2026, as part of the National Report on Tech and Innovative Companies 2026.

UPDATE LINKS

Ecosystem Evolution

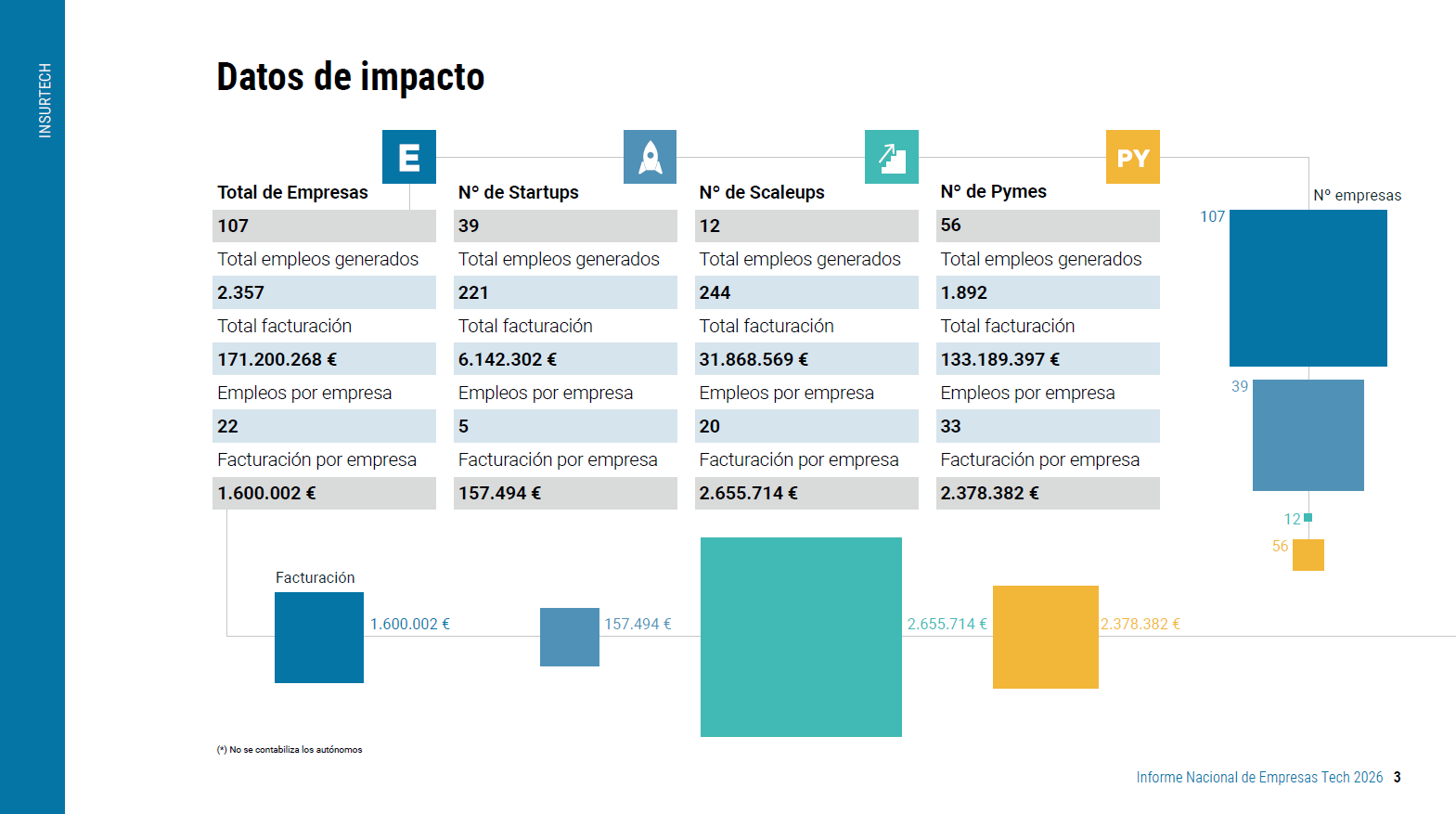

The insurtech ecosystem in Spain is comprised of 107 companies, generating a total of 2,357 jobs and achieving an aggregate turnover of 171,200,268 euros. On average, each company has 22 employees and an approximate turnover of 1,600,002 euros, which helps to gauge the sector's economic significance within the insurance industry. These figures reflect a consolidated business fabric, capable of generating economic activity and employment.

Ecosystem Snapshot

The ecosystem analysis distinguishes three types of companies based on their level of maturity and development.

- Startups, which represent 39 companies, generate 221 jobs and a turnover of 6,142,302 euros, with an average of 5 employees per company.

- Scaleups, with 12 companies, employ 244 people and generate €31,868,569 in revenue, significantly increasing the average volume per company.

- Meanwhile, SMEs, which make up the majority group with 56 companies, employ 1,892 people and generate €133,189,397 in revenue.

These categories show differences in terms of employment and revenue, with SMEs concentrating the largest aggregate volume of both indicators.

Geographical distribution

The report identifies Madrid as the main hub of the insurtech ecosystem in Spain, with 42 companies, 826 employees and €69,410,758 in revenue. Barcelona ranks second with 17 companies, 269 employees, and €27,213,968 in revenue. Alongside these cities, the ecosystem extends to other regions such as Valencia, Seville, Malaga, and A Coruña, showing a distributed presence, albeit concentrated in major urban centers.

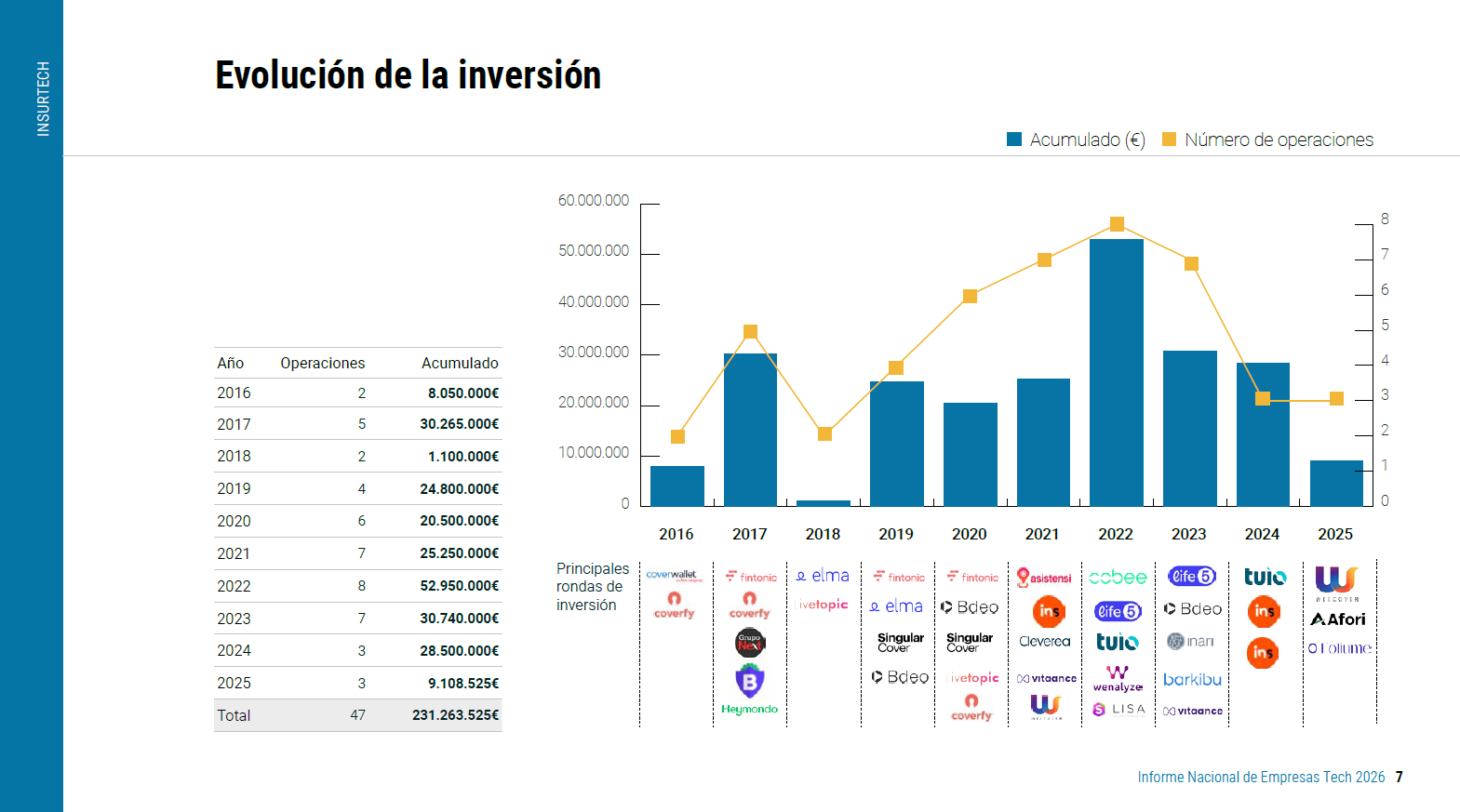

Investment

The ecosystem has accumulated a total of €231,263,525 in investment distributed across 47 operations. Annual evolution shows significant differences between years, with a peak of €52,950,000 in 2022, followed by €30,740,000 in 2023 and €28,500,000 in 2024. In 2025, investment decreased to €9,108,525 distributed across 3 operations: Weecover, Afori, and Foliume. Notable rounds from companies such as Cobee, Fintonic, Tuio, Life5, and Bdeo are highlighted in the report.

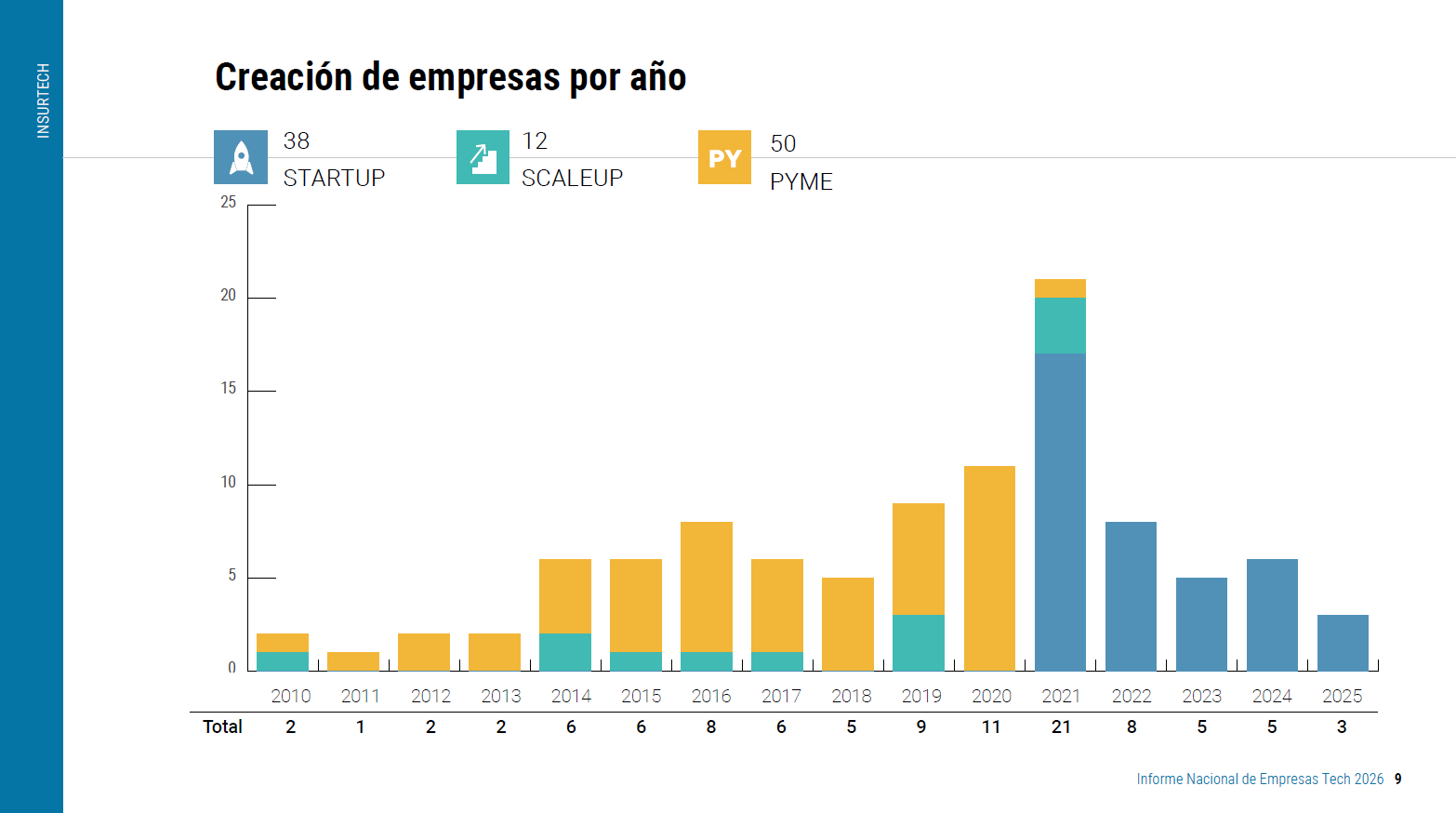

Company creation

The evolution of company creation reflects different phases since 2010. The number of new companies peaked in 2021 with 21 companies and has progressively decreased to 3 new companies in 2025. These data indicate a slowdown in the pace of creation over the last few years analyzed.

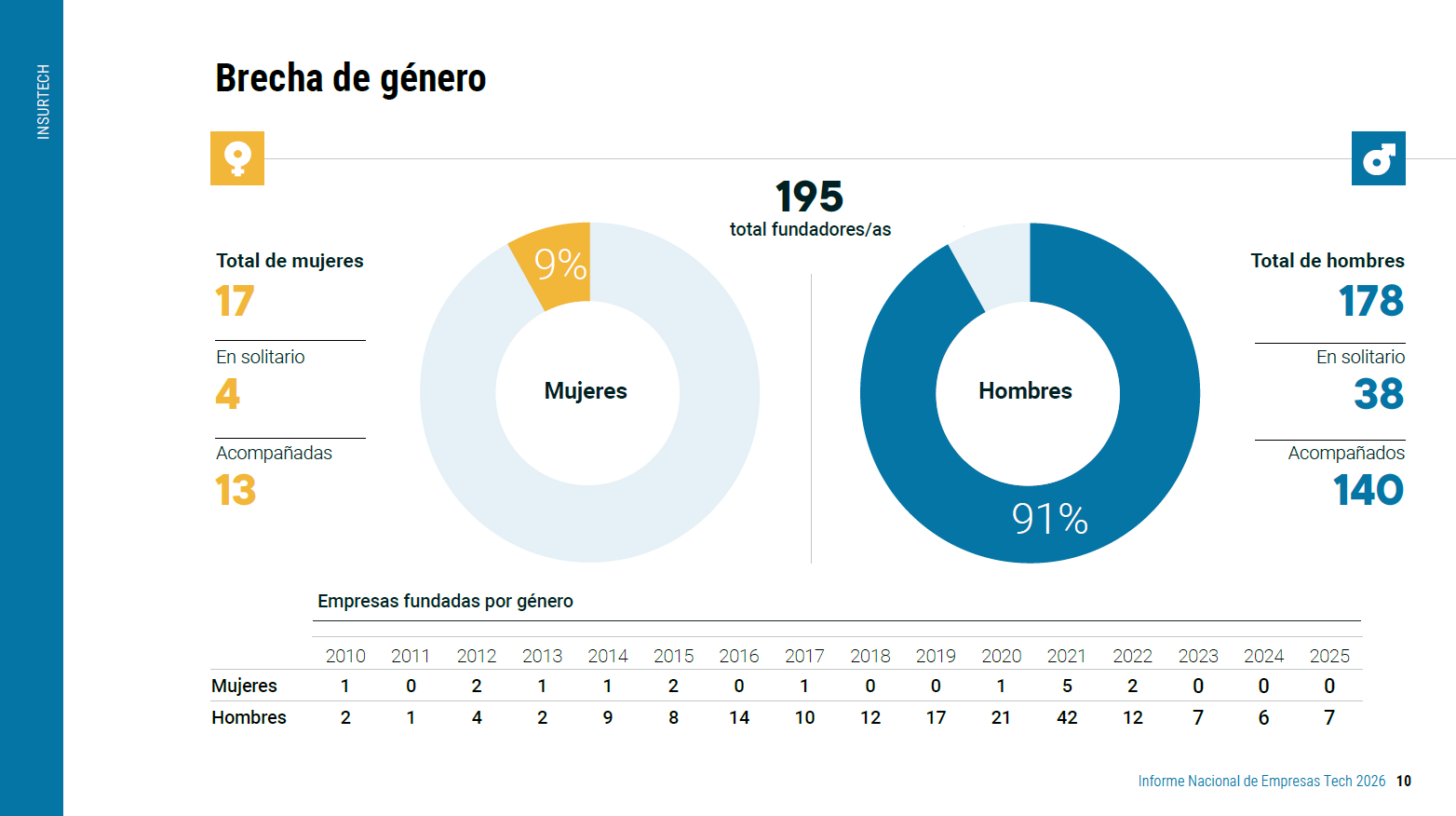

Founder profile

The report identifies a total of 212 founders in the ecosystem, of whom 195 are men and 17 are women. In percentage terms, this represents a distribution of 91% men versus 9% women, highlighting a significant gender representation gap within the sector.

The Role of Santalucía Impulsa

Within the scope of the report, Santalucía Impulsa positions itself as a key player in connecting startups and business within the Group, promoting an open innovation model aimed at generating real value. This approach focuses on collaborating with startups to address specific business challenges, prioritizing strategic fit, execution capability, and tangible impact. It also reflects an evolution towards initiatives with a scaling ambition, where innovation is directly integrated into areas such as customer experience, operations, data, and new service development.

Conclusions

- The insurtech ecosystem in Spain comprises 107 companies that generate over 2,300 jobs and €171 million in revenue.

- The sector's economic impact is driven by more developed companies, SMEs, which account for the majority of the economic impact and employment within the sector.

- Madrid is positioned as the main hub of the ecosystem, followed by Barcelona, the two dominant poles with a high concentration of activity.

- The cumulative investment exceeds €231 million, with significant variations between years.

- The creation of new insurtech companies has seen a reduction during the last few years analyzed.

- An unequal distribution persists in the founder profile, with 91% men and 9% women: gender diversity remains a structural challenge for the ecosystem.

- Artificial intelligence is consolidating as a strategic priority, although with limited economic impact in most companies: there is a gap between adoption and return